Investor attention each earnings season tends to tilt heavily toward the biggest tech stocks. But with 3 of the top 10 holdings of the $38 billion Health Care Select Sector SPDR Fund ETF (NYSEARCA:XLV) reporting earnings this week, and 5 of the “Magnificent 7” stocks having reported already, this has potential to be a key week for a sector that could draw more attention.

That’s because healthcare has traditionally been considered a “flight to safety” sector, filled with companies that operate business that produce products and services considered essential. These business leaders also benefit from the US healthcare system having evolved toward a smaller group of dominant players in their fields. Add to that the ongoing intrigue from the surge in interest in “GLP-1 receptors,” a class of drugs that have taken the business world by storm, since they gained attention and acceptance for their dramatic results as weight loss medicines.

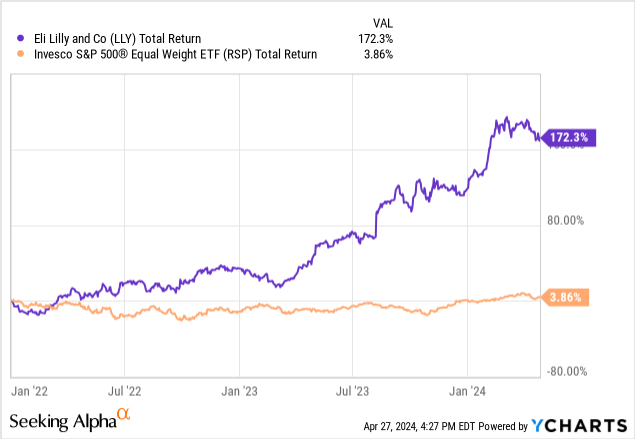

While still extremely new and thus controversial, one of the top GLP-1 providers, Eli Lilly and Co. (LLY), has rocketed up the market cap charts in a way that has left any short sellers feeling as light in their wallets as many Ozempic patients feel in their bodies. As shown here, since the start of 2022, the average S&P 500 stock is up a total of less than 4% in 28 months. LLY is up 172%, putting it in the top 10 of the S&P 500.

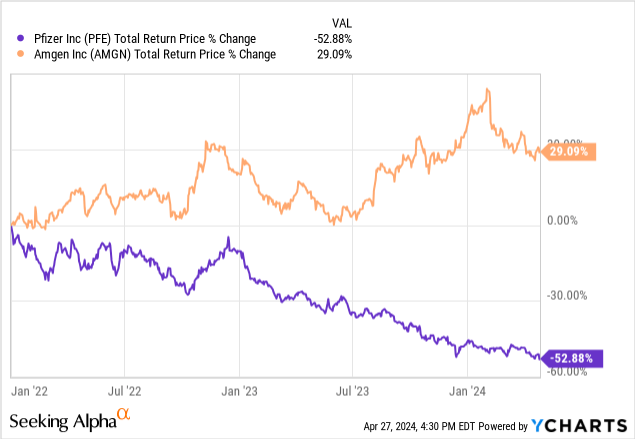

Pfizer (PFE) and Amgen (AMGN) also report this week, and each makes up about 3% of XLV. These two have gone in totally opposite directions since the start of 2022, and both were members of the Dow Jones Industrial Average, but PFE was dropped from the Dow back in 2020.

If this seems like it paints a diverse and volatile picture for the formerly mundane healthcare sector, that’s because it does. Competition, regulation, and the dominance of tech stocks have all played a role in that. So, now what?

XLV: an ETF tracking large cap healthcare stocks in the S&P 500

XLV debuted way back in late 1998, making it one of the oldest ETFs. It is one of a set of 11 State Street issued back then to track the 11 sectors of the S&P 500. The SPDR S&P 500 ETF Trust (SPY) started the US ETF industry in 1993, and these 11 “Sector “Spiders” came along and allowed investors to break up that single index fund into sectors.

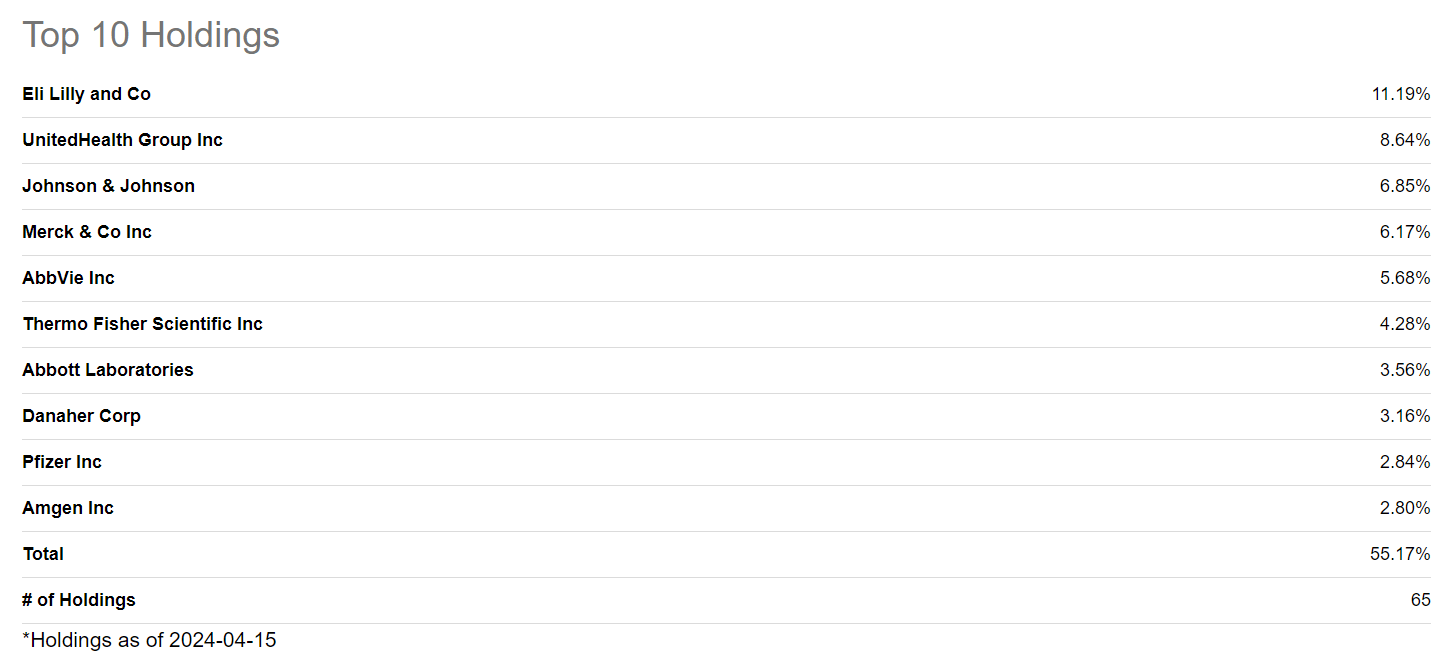

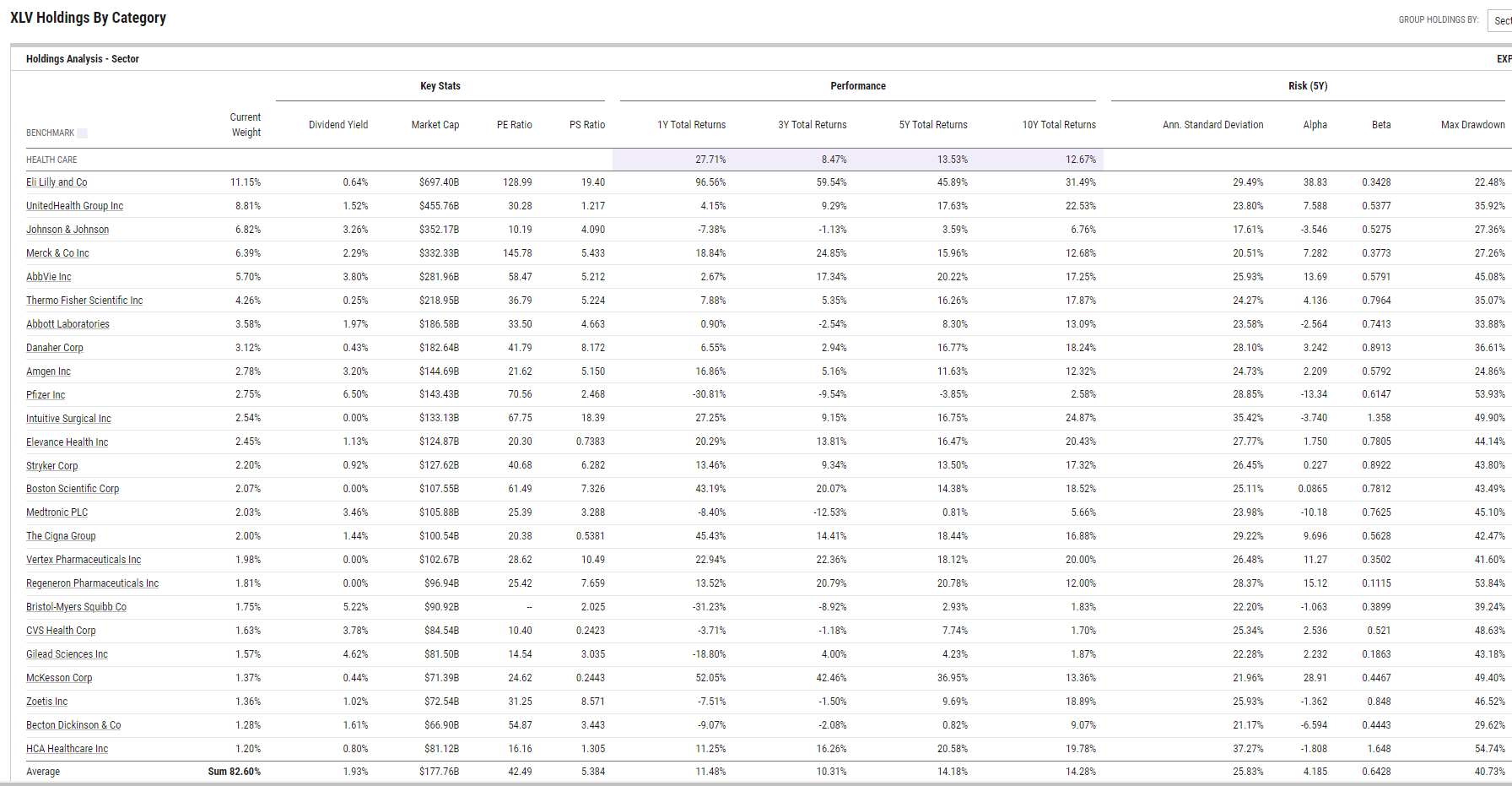

XLV owns all 65 tracks health care stocks from within the S&P 500 Index, weighted by market capitalization. This includes pharmaceutical stocks, health care equipment companies, health care plans like UnitedHealth Group (UNH), biotechnology, life sciences healthcare technology stocks.

The top 10 holdings, shown below, offer a bit of most of those. However, as is the case for 10 of the 11 sector SPDR ETFs (all except Industrials), XLV is quite top-heavy, with 55% of assets in the top 10 stocks and 82% made up by the top 25. So, 40 stocks only comprise 18% of the ETF. I actually prefer this, since a sector ETF like this is always going to be a slice of my portfolio, not the majority of it.

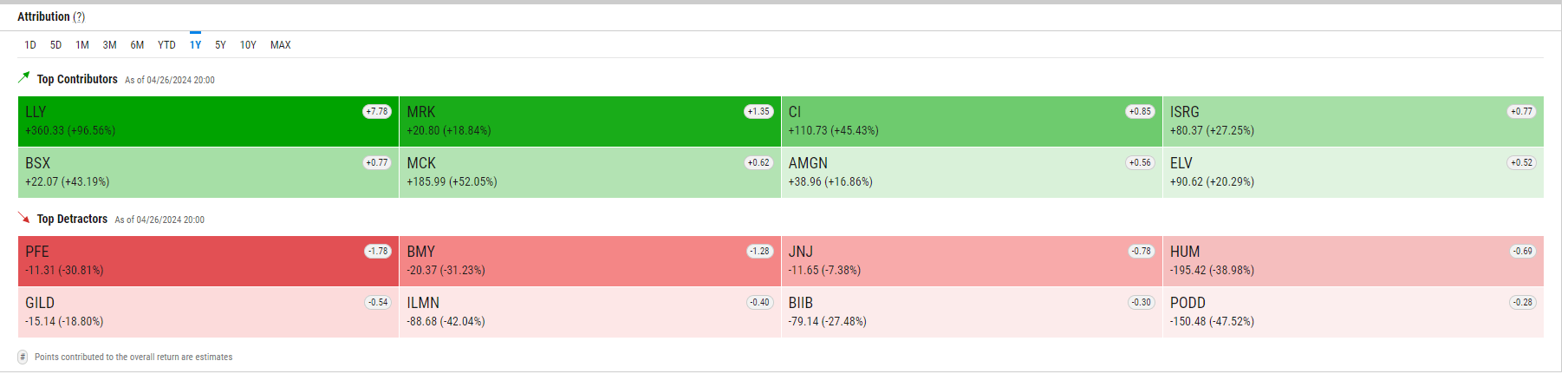

Below, we can see that LLY has been the dominant source of alpha for the past 12 months. In fact, XLV is up about 8% during that time, and LLY has contributed 5.6% of that 8%. That’s 70% of the return from one big weight loss juggernaut! As such, I always evaluate XLV with one eye toward what LLY is doing. AMGN, reporting this week, has been a source of alpha the past year, while PFE has been the leading performance detractor, along with Bristol Myers (BMY) and Johnson & Johnson (JNJ).

And that indicates just how the nature of large cap healthcare investing has changed. Those 3 stocks used to be the icons of the sector. Now, they are holding it back, at least in the recent past. Their potential revival has to be part of an investor’s comeback case for XLV.

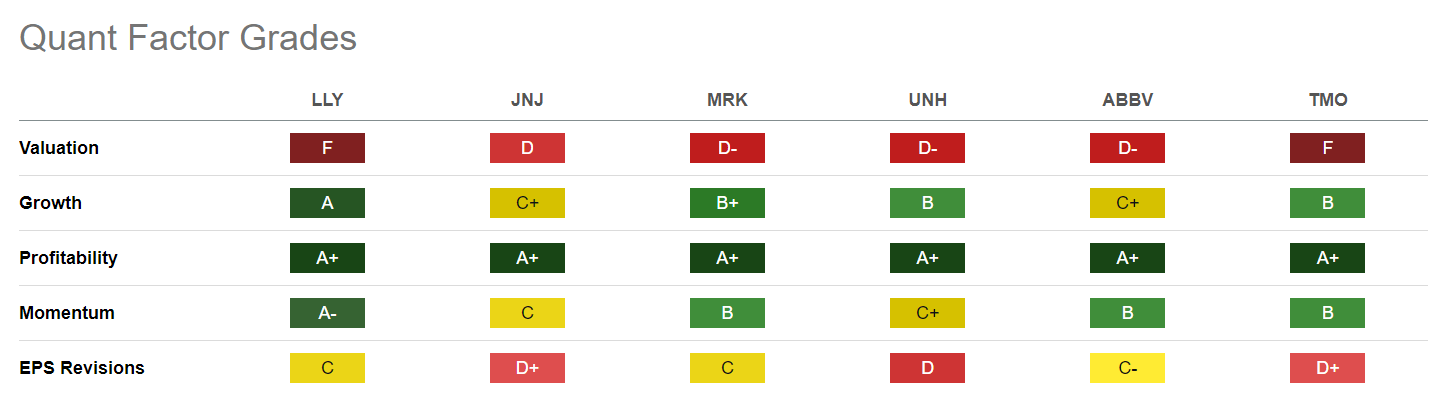

XLV: analysis of Seeking Alpha Quant Factors

Here are 6 of the top holdings, which account for 43% of XLV’s total assets. Those are some discouraging valuation grades, which I think speaks of the overvaluation of US large caps in many sectors versus everything else. Earnings are being revised down more than up, and growth has been mixed.

The saving grace for this sector, and why I follow it closely even at times like this where I am not very involved in it, is the solid profitability that is a staple of the healthcare businesses that make up most of XLV. That has afforded them premium valuation multiples over the years, and it is why my preference will be to take up my allocation to healthcare stocks when everything is a lot cheaper. There are plenty of other sectors to choose from.

That said, I will have multiple stocks from this sector in the 40-stock portfolio I am building. I’m just keeping the position sizes quite low for now. I currently own PFE, BMY and Baxter (BAX) in small amounts.

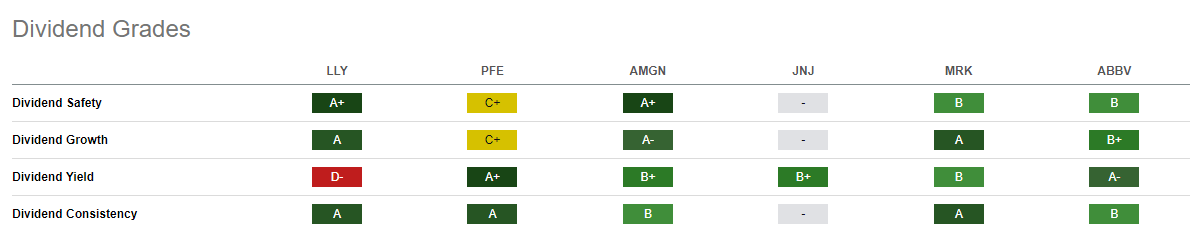

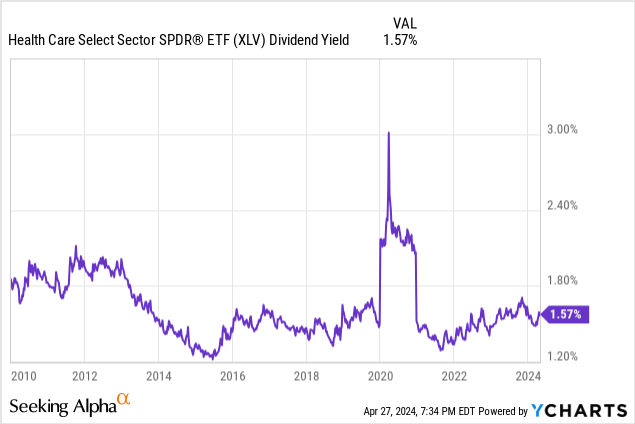

A solid dividend yield is something else healthcare investors could count on in years past. They still can, but at the index level, when capitalization-weighted, that yield is only around 1.5%. These same stocks in equal-weighted allocation yield about 2.2%.

Here’s a look at the top 25 in more detail, to drive home some of the observations I made to this point. There are a lot of low beta names in here. But for a while now, those traditional safe havens have been overshadowed by high flyers.

Technicals: nothing special here

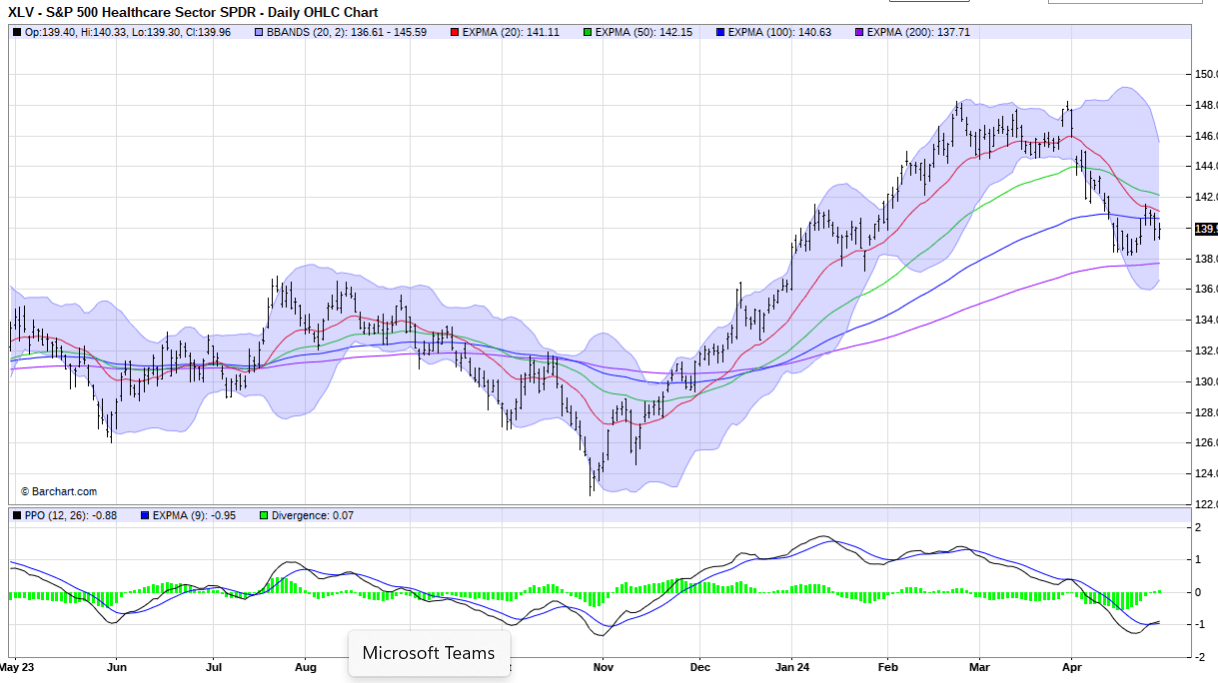

I would not expect XLV’s chart to look anything more than hopeful, since I find it nearly impossible to identify US large cap stocks in any sector that have more than a “puncher’s chance” of significant upside from here. That might change, but I’d rather see a lot more than I see currently.

This chart of daily prices indicates to me that XLV is hanging on, rather than preparing for a big run higher. The 20-day and 50-day moving averages are downward-sloping, though there is at least a possibility that XLV could find a double-bottom in the $138 area. But that’s just me trying to reach for a positive. Perhaps this week’s key earnings announcements will spark a change in this trend, one way or another. LLY’s chart, not shown here, is in what I judge to be an earlier stage decline than XLV itself. That adds to the malaise I see here, technically speaking.

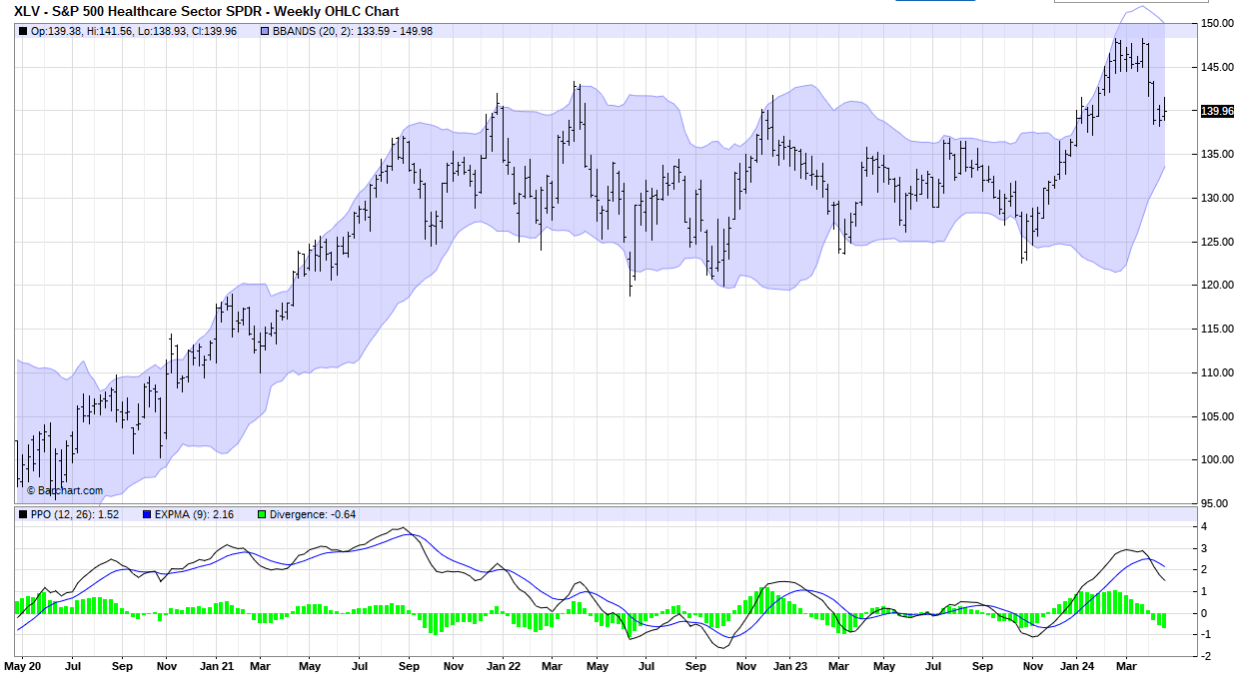

Finally, the XLV weekly chart does not show much different, other than that shaded area (Bollinger Bands) marketing a potential downside target in the $125-$120 range.

Conclusion: Hold on XLV (a weak one at that)

I am frankly neutral on this sector, but I do expect there’s a good chance that it will be a leader coming out of the next recession, as it typically is. But one step at a time. There’s no recession yet. So for now, with little box-checking in terms of my favorite pieces of a good reward/risk tradeoff, technically and fundamentally, I am keeping healthcare stocks at the back of my watchlist, and lightly weighted in my 40-stock portfolio for now.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of PFE either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I own a small position in a larger portfolio in each of PFE, BMY and BAX from this sector

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.