Amazon Earnings

Last week, Alphabet (GOOG, GOOGL) and Microsoft (MSFT) saved the market after it had started moving south after a stellar quarter. Blow-out earnings excited investors, who bid both companies up 10 and 5 percentage points, respectively.

Both reports and earnings calls were extremely interesting and bullish, leaving investors impressed that AI is, of course, only in its early stages.

But what I think is more relevant is that both companies released some important data that makes it easier for us to predict Amazon’s (NASDAQ:AMZN) earnings. More in detail, I believe Amazon’s quarterly report will be great.

Here is why.

Google: Ads And Cloud Driving Revenue

Alphabet’s press release was clear: Google is growing and delivered revenues of $80.5 billion, up 15% year-on-year, coupled with operating margin expansion. Investors cheered.

What drove these outstanding and somewhat unexpected results? During the earnings call, Sundar Pichai was clear when he started guiding for the full fiscal year: “We expect YouTube overall and Cloud to exit 2024 at a combined annual run rate of over $100 billion”.

In other words, ads and the cloud are performing great.

As a matter of fact, Google reported $61.66 billion in revenues under advertising (Google Search, YouTube ads, Google Network, and others), while Google Cloud reached $9.57 billion in revenues. The former was up 13% YoY, while the latter surged 28% YoY.

Even more striking, Google reported that

as of March 31, 2024, we had $72.5 billion of remaining performance obligations (“revenue backlog”), primarily related to Google Cloud. Our revenue backlog represents commitments in customer contracts for future services that have not yet been recognized as revenue. […] We expect to recognize approximately half of the revenue backlog as revenues over the next 24 months with the remaining to be recognized after that.

If Google stopped its customer acquisitions, it would still have $9 billion in Cloud revenue per quarter for the next two years. Of course, this is only the floor on top of which we should expect further and sustained growth.

Google Cloud also reported an operating income of $900 million and an operating margin of 9%.

Shifting to ads, Google’s management openly talked about strong momentum. In particular, APAC-based retailers are spending, but big retail customers also found Google a valuable partner. This is what was said during the earnings call about IKEA, for example:

In Q1, retail was again a top contributor. Our focus remains on driving profitability and growth for retailers, helping them optimize digital performance for both online and offline, as well as innovate across our shopping and merchant experiences. Highlights include continued upsides for retailers, leading into agile budget and bidding strategies across Search, P-Max, or both. Take Home Goods retailer IKEA, who leaned into Google’s store sales measurement to understand its total omnichannel revenue opportunity across Search. By measuring 2.3x more revenue and using value-based bidding solutions to bid to its omnichannel customers, IKEA drove a significant increase in Omni revenue in Q1 and is now scaling this strategy globally.

YouTube is also becoming a true golden goose when speaking of ad revenue. It is currently the number one platform in the U.S. for streaming, with over 1 billion hours of YouTube content on TVs daily. Google also announced YouTube surpassed 100 million premium subscriptions, with YouTube TV topping 8 million subscribers.

Ads were strong, with shorts monetization improving and doubling in just 12 months. In Q1, Google also talked about “strong traction from the introduction of a Pause Ads pilot on connected TVs, a new non-interruptive ad format that appears when users pause their organic content”.

The final treat for investors was the announcement that Google, in addition to its $70 billion buyback program, will return money to its shareholders via its first-ever quarterly cash dividend to be paid in June.

We delivered a free cash flow of $16.8 billion in the first quarter and $69.1 billion for the trailing 12 months. We ended the quarter with $108 billion in cash and marketable securities.

Microsoft: Azure And Ads Grow Fast

While Google sees its main strength in ads, with its cloud business still scaling up, Microsoft is the other way around. Azure is well-established and is second only to AWS. On the other hand, the company still has a lot to explore when considering advertising.

In Microsoft’s Q1 Earnings Presentation, we see that search and news advertising revenue increased 12%. LinkedIn revenue increased 10%. Microsoft reported, therefore, $4 billion in revenue from LinkedIn and another $3.13 billion from Search and news advertising. Small numbers compared to Google’s. But the growth rate is quite good.

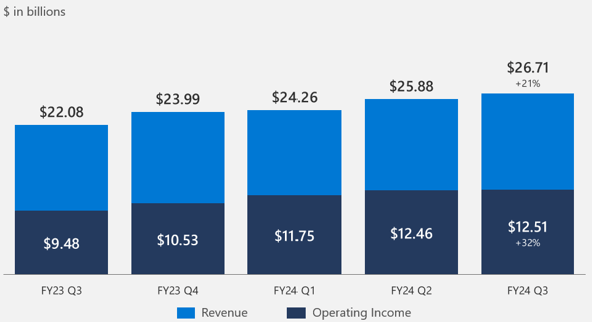

On the other side, Microsoft’s revenue in Intelligent Cloud was $26.7 billion and increased 21%, with server products and cloud services revenue up 24% YoY, thanks to Azure and other cloud services revenue growth of 31%.

Here is Microsoft’s Intelligent Cloud business’ revenue growth: quarter after quarter we see a steady upward trend.

Of course, both Microsoft and Google talked about AI and the huge benefits they and their customers are seeing from the first implementation of this new technology into their existing products and services.

Amazon’s Earnings Report

So, from Google and Microsoft we know that advertising is currently performing well and that cloud is accelerating again. This has a big impact on Amazon since two of its main business lines are indeed advertising and AWS. If we leave aside Amazon’s retail business (both first and third-party sales), AWS and ads are the largest two contributors to Amazon’s revenues, with $90.76 billion made by AWS in 2023 and $46.91 billion grossed by ads services.

In its 2023 shareholder letter, Andy Jassy pointed immediately out that Amazon’s pivot to profitability is proving to be great:

Amazon’s operating income and Free Cash Flow dramatically improved. Operating income in 2023 improved 201% YoY from $12.2B (an operating margin of 2.4%) to $36.9B (an operating margin of 6.4%). Trailing Twelve Month FCF adjusted for equipment finance leases improved from -$12.8B in 2022 to $35.5B (up $48.3B)

More in detail, at the end of FY 2023, Amazon reported ads growth of 24% YoY. And this was achieved while sponsored TV had just been added, which is a self-service solution for brands to create their marketing campaigns and have them appear on several streaming TV services. Amazon is also expanding its TV ads, introducing ads into Prime Video. With these new uses of ads, we can bet Amazon is going to report ads revenue above expectations. My guess is that we could see Amazon report 18% ad growth YoY, which would make Amazon come close to $11.4 billion in revenue.

Mr. Jassy, in its shareholder letter, also addressed Prime Video, saying Amazon is convinced that it can become “a large and profitable business on its own”. If we think about it, Prime Video is set to have great success in ads. After all, who better than Amazon knows its members’ profiles and preferences, thus being able to surgically target each ad to the most convertible Prime members? Indeed, in media and ad

Shifting to AWS, Mr. Jassy spent a few pages describing how Amazon’s Web Services is built on primitives, basic building blocks, or services that can be then used and combined by anyone to create more complex systems or apps. I suggest reading those pages if you have never heard about this business model Amazon follows. Primitives are extremely important to enhance AWS’ customer experiences. In particular, there are a lot of primitives to be built since GenAI has made its appearance.

Given Google’s and Microsoft’s strength in the cloud, I am inclined to think AWS will overdeliver, too and I think a 17% YoY growth may not be so far from the truth. This would make AWS report a quarterly revenue of $25 billion, which means we are going to see it surpass $100 billion by the end of the fiscal year. Impressive.

But what is even more striking is what Amazon has been able to do in just a few quarters since it started ramping down its last investment cycle right after COVID-19.

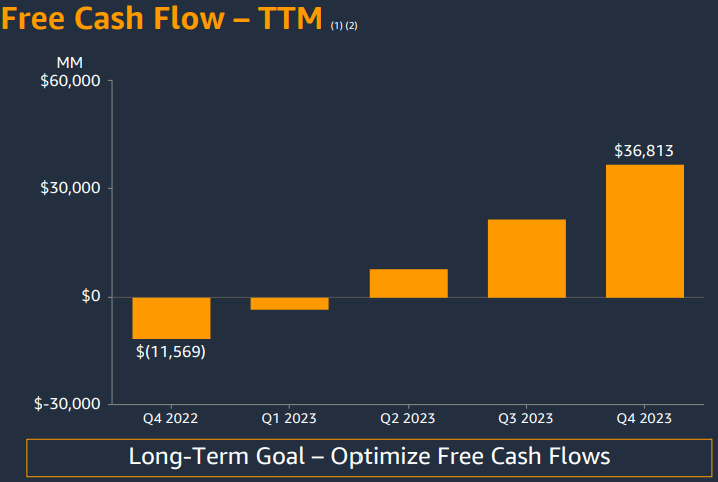

In Q1 2022, Amazon reported $-18.63 billion in FCF for the trailing twelve months. At the end of Q4 2023, Amazon’s TTM FCF was already $36.81 billion. This is an increase of over $55 billion in just seven quarters.

Considering Amazon’s capex is decreasing a bit, we could have a TTM capex below $50 billion. At the same time, Amazon’s TTM operating cash could come well above $90 billion. This means I am expecting Amazon to report at least $40 billion in TTM FCF. But I think this is a conservative estimate and I wouldn’t be surprised to see Amazon report an additional $4-5 billion in TTM FCF.

However, Amazon has guided for a YoY Capex increase this year due to increased infrastructure and genAI spending. As a result, I am not forecasting Amazon’s capex will dip below $50 billion at the end of FY2024. But Amazon’s cash from operations is growing fast and by the end of the year, it could come close to $100 billion. As a result, I believe Amazon will report $50 billion in FCF at the end of FY 2024. This means Amazon is trading at a fwd FY24 FCF yield of 2.7%. This is no big steal, but it is also not extremely expensive. Considering Amazon has just started focusing on its profitability metrics, I would not be surprised to see it report in a year or two $100 billion in FCF, which would make the company trade at a 5.3% FCF yield.

With these numbers, I think Amazon will soon go along with Google and instate a dividend, too. I am not expecting this right away because Amazon has always said it would rather spend and invest in its own business. But, sooner or later, if its ability to generate FCF proves true, the company will have so much cash that it won’t know how to use it.

Now, if Amazon reports 17% growth in cloud and 18% growth in ads, we would have the company’s overall earnings come above the current revenue estimate of $142.5 billion. We could probably see a report of $145 billion, which would be a 13.9% growth YoY. I have a hard time believing investors would not bid up Amazon’s price if these numbers were reached by Amazon.

Given the tailwinds that Google and Microsoft reported, I think Amazon will be a strong beneficiary of these trends. As a result, even though Amazon is close to its ATHs, I rate it as a buy.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMZN, GOOG, MSFT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.