In this article, we will take a look into Meta Platforms Inc’s (NASDAQ:META) DCF analysis, a reliable and data-driven approach to estimating its intrinsic value. Instead of using future free cash flow as in the traditional DCF model, the GuruFocus DCF calculator uses EPS without NRI as the default for the DCF model based on research that shows that historically stock prices have been more correlated with earnings than free cash flow.

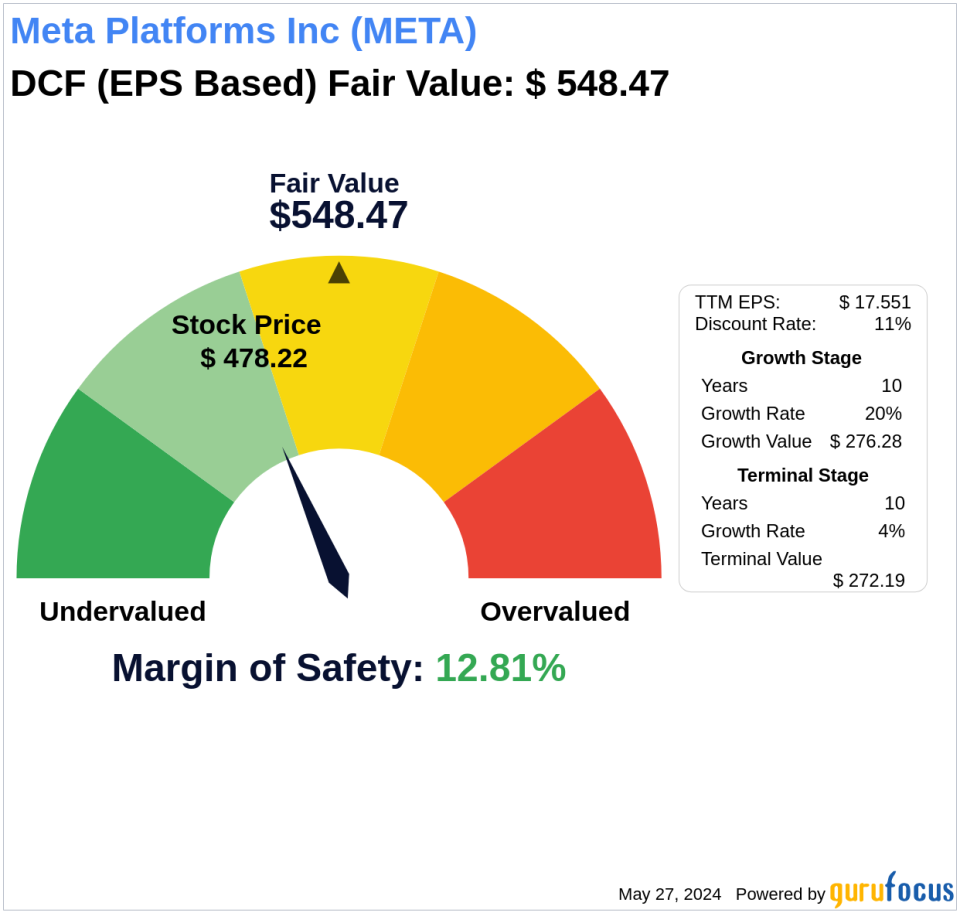

As of 2024-05-27, Meta Platforms Inc’s intrinsic value as calculated by the Discounted Earnings model is $548.47. It’s currently trading at a price of $478.22. Therefore, the margin of safety based on the DCF model is 12.81%. The company is modestly undervalued.

The model

The GuruFocus DCF calculator follows a two-stage model by default. This model consists of the Growth Stage and the Terminal Stage. In the growth stage, the company is experiencing faster growth, while in the terminal stage, a lower growth rate is applied because sustained rapid growth is not sustainable in the long run. Meta Platforms Inc’s intrinsic value estimated by Discounted Earnings model are arrived at by following assumptions and steps.

Assumptions

Calculation

Discounted Free Cash Flow Model

GuruFocus also provides the calculation using the traditional approach of free cash flow. Using trailing twelve month(ttm) Free Cash Flow per Share as a parameter, the DCF intrinsic value based on free cash flow is $588.03. This valuation indicates that the Meta Platforms Inc is modestly undervalued, accompanied by a margin of safety of 18.67%. You can always switch to using Free Cash Flow per Share to calculate the real DCF model on our DCF calculator page.

The Bottom Line

Please note that while the DCF model is a robust valuation methodology, it relies on various assumptions and projections that may affect the accuracy of the final intrinsic value calculation. Here are some considerations when employing the DCF model:

- Future Earnings Potential: The DCF model evaluates a company based on its potential future earnings.

- Embracing Growth: Growth plays a pivotal role. All else being equal, a company with rapid growth will have a higher value.

- Predictability: The model assumes that a company will grow at the same rate as its past 10-year performance, making it a better fit for companies with consistent performance. For companies with unpredictable performance, such as cyclical companies, the DCF model may be less accurate and a larger margin of safety should be emphasized.

- Discount Rate: Selecting an appropriate discount rate is paramount. Using your anticipated return on investment is a sensible choice for the discount rate.

Navigating with GuruFocus:

Using the GuruFocus All-in-One Screener, you can easily screen for stocks that are currently trading below their intrinsic value: DCF (FCF Based) and Intrinsic Value: DCF (Earnings Based). To identify undervalued predictable companies, focus on those with a high Predictability Rank that are trading at a discount to their Intrinsic Value: DCF (FCF Based) and Intrinsic Value: DCF (Earnings Based).

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.

This article first appeared on GuruFocus.