I presented my bullish view on Costco Wholesale Corporation (NASDAQ:COST) in my previous coverage published in March 2024, favoring its strong membership growth and potential to raise its membership fees. The company released its Q3 FY24 result on May 30th after the bell, with 6.5% adjusted same-store sales growth and 8% membership fee growth. I maintain the “Buy” rating with a fair value of $870 per share.

Strong e-Commerce Growth driven by Discretionary Purchases

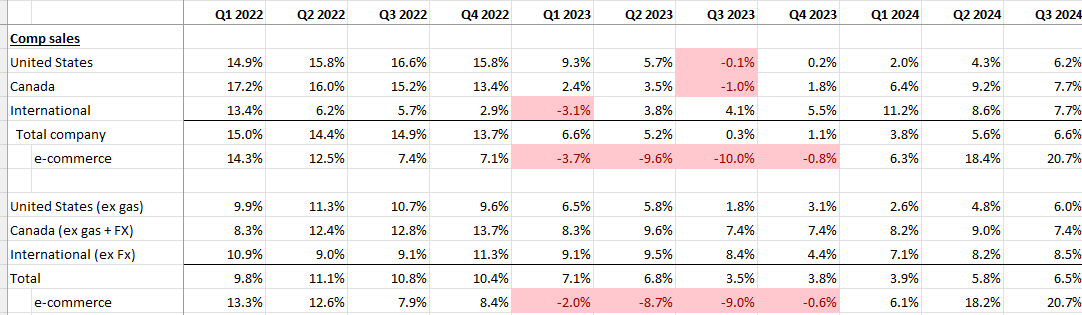

My biggest takeaway from this quarter is their strong e-commerce growth, which delivered 20.7% growth in the quarter, as depicted in the table below. The strong growth is driven by two main factors:

- Costco’s e-commerce business was weak throughout FY23, due to weak sales in large-ticket discretionary items. As such, the company has been facing weak comparables in FY24.

- As communicated over the earnings call, Costco has experienced strong growth in Gold and Silver bullion, gift cards and appliances. More specifically, appliances grew by 30% year-over-year. Costco has done an impressive job of lowering product prices to add value for its members.

The strong growth in e-commerce is quite notable for Costco, as the digital channel possesses a much better margin for Costco. The fast growth in e-commerce could potentially drive Costco’s margin expansion over time.

Partnership with Uber Eats

Costco is available on Uber Technologies, Inc. (UBER) Eats in select locations across the U.S., Canada, Mexico, and Japan, and Costco is expanding the partnership into more regions in the coming months. The partnership could be a win-win situation for both companies. Key reasons are:

- Uber One has 19 million members at the end of Q1 FY24, and Costco has 34.5 million paid executive memberships. The partnership could potentially cross-sell gift cards and other products on both platforms.

- Costco is testing the grocery delivery through Uber Eats in some regions like Texas. After meeting some conditions, the ordered groceries could be delivered within several hours. Uber One members can access Costco’s merchandise even without a Costco membership. The grocery delivery service could potentially help Costco gain more customers, especially among younger customers who favor grocery delivery.

FY25 Outlook

After the growth volatility caused by the global pandemic, I anticipate Costco will gradually normalize its growth, as discussed in my previous coverages. For its FY25’s growth, I am considering the following factors:

- As the inflation begins to subside, I anticipate the Fed will start to cut the interest rate this year, which could benefit consumer consumption. Costco has been leveraging its Kirkland brand to lower the merchandise price. As hinted during the earnings call, the Kirkland brand has a goal to achieve at least 20% value compared to branded products. When the interest rate begins to get cut, it is most likely that Costco will benefit from the improving consumption.

- I anticipate Costco’s e-commerce will grow at a double-digit rate. Costco possesses the advantages of offering both online and offline channels. Additionally, their partnership with Uber could potentially accelerate their e-commerce business in the near future.

As such, I continue to anticipate Costco can deliver 6% comparable sales growth in the near future, assuming 5% growth from retail stores and 1% growth from e-commerce. Additionally, as mentioned in my previous coverage, Costco has not raised its membership fee for several years. The potential fee increase could contribute additional profits for the company.

Valuation

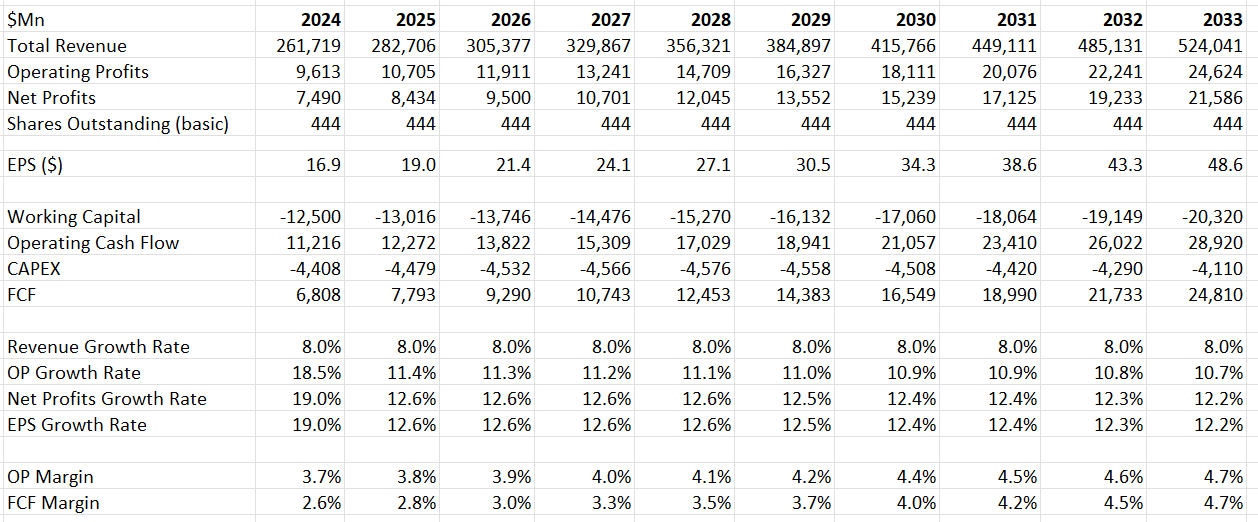

Costco anticipates reaching 890 stores at the end of FY24, and the warehouse expansion could contribute an additional 2% growth to the top line, as per my calculations.

As discussed, I predict Costco will generate 6% comparable sales growth. As such, the total growth rate is assumed to be 8% in the model.

Costco’s margin expansion is driven by several factors:

Membership fee growth: the membership fee grew by 8% in the quarter. As the majority of incremental fee income will drop to the bottom line of P&L, leading to notable margin expansion for the company. I anticipate the strong membership growth will continue in the future, considering the value added to its members.

In addition, Costco can enjoy the operating leverage from their gross profits and SG&A expenses. I calculate that Costco will expand their operating margin by 10bps annually, driven by 5bps from gross margin and 5bps from SG&A.

The WACC is calculated to be 9.1% assuming:

- -Risk free rate: 4.25% (US 10Y Treasury Yield).

- -Beta: 0.84 (SA).

- -equity risk premium 7%; cost of debt 7%.

- -debt balance: $6.4 billion; equity $25 billion.

- -tax rate: 26.5%.

Discounting all the future free cash flow and adjusting the net debts, the fair value of Costco is estimated to be $870 per share.

Risks

I don’t think Costco’s business contains any significant risk factors. Instead, their high stock price multiple might cause market concerns. However, I want to point out that the traditional P/E multiple might not be a good indicator of its intrinsic value for the following reasons:

- Costco is a quite low volatility stock with a beta of 0.84. The lower beta would result in a low discount rate for their stock price calculations.

- Costco performed well during the last recession in 2009, declining only 1.1% in total revenue. The business outperformance during recessions is favored by institutional investors.

- It would be hard for any competitors to replicate Costco’s business model, and basically, Costco’s biggest competitor is themselves.

Conclusion

I favor Costco’s strong membership and e-commerce growth. The company’s continuing efforts to lower merchandise prices make the company quite unique in the retail industry. I maintain the “Buy” rating with a fair value of $870 per share.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of COST either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.