The legendary Warren Buffett’s single biggest holding by a mile is Apple (NASDAQ: AAPL). The iPhone maker makes up 43% of Berkshire Hathaway‘s portfolio — close to $170 billion in AAPL stock.

After Berkshire’s last annual meeting, Buffett said that Apple “is an even better business” than his long time favorites, Coca-Cola and American Express. Although he sold off some shares over the last year, Buffett insisted that this was for tax purposes, not because he lost faith in the company. If you want a reason to believe in Apple, you could do worse than to look to the Oracle of Omaha.

But let’s dive deeper; it’s not an entirely rosy picture for the company. Apple lost some of its sheen in the last year after disappointing iPhone sales in China and at home. The company was also slow to capitalize on the hype of artificial intelligence (AI).

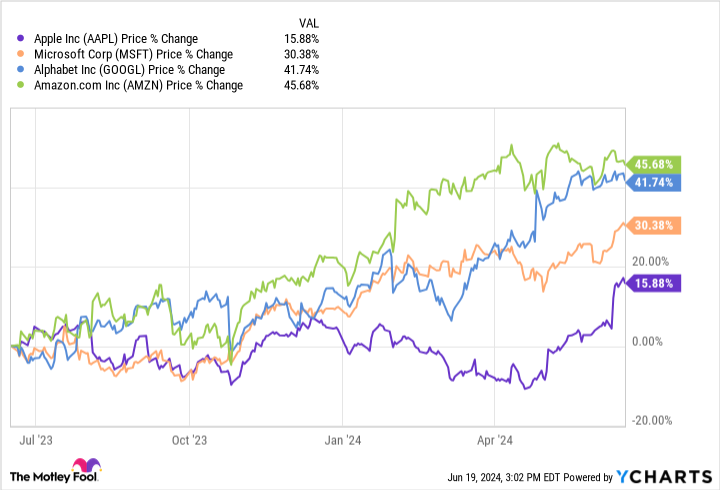

Some investors feared Apple had gone soft, falling behind in both its core business and a new one. While its stock is up over the last year, its growth was limited compared to its peers. Take a look at this chart showing just how much:

Despite some worrying trends, the company has reversed the narrative as of late. Here are three reasons Apple is still a force to be reckoned with.

1. People were too quick to count Apple out of AI

Although it’s too early to truly tell, AI could have a revolutionary power on par with the internet. After ChatGPT exploded onto the scene, investors looked to each leading tech company to see what it would offer the public. Many companies jumped in quickly, releasing their own chatbots or AI integrations, and using the term “AI” as many times as they could reasonably fit into a coherent sentence.

Apple was conspicuously absent from this early rush, spooking investors who believed it would be left in the dust. Now that looks like a tactical move, by a company that built its reputation on products that work and work well. The sleek design its products are famous for and that others attempt to emulate — or straight-out copy, like the private Chinese company Huawei — comes from a general philosophy guiding everything the company does. Apple wants to make sure it does AI right.

Compare that to Google parent Alphabet‘s approach: The Apple rival fell on its face at least three times, by my count, since releasing its AI offerings. Since jumping into the ring early in 2023, Google’s AI products, Bard and Gemini, have been plagued with high-profile issues.

Apple, in contrast, waited until it was ready, finally revealing the cleverly named Apple Intelligence to the world earlier this month; its features look quite impressive. Although we’ll have to wait and see just how well it works, the market reacted well to the news, believing Apple finally showed it has a worthy AI offering. The stock is up about 10% since.

2. iPhone sales rebounded in China, and Apple Intelligence may spur sales domestically

Although numbers aren’t where the company want them to be, iPhone sales in China do look to be headed in the right direction. A report out of China last month showed that foreign-made smartphone sales rose 52% from the same period a year earlier. Apple is not the only company that qualifies as foreign, but it is by far the largest. It cut prices to better compete with Chinese rivals, and that appears to be working.

At home, although sales are still lacking, the release of Apple Intelligence may be the catalyst the company needs to get back on track. The technology will only run on newer models, which means customers who want in on AI capabilities will be forced to upgrade to the latest hardware. While it’s hard to put a number on how many will fall into this camp, I think a significant portion will. That may be enough to drive sales for some time.

3. Growth in the services segment is setting records

Apple doesn’t just sell iPhones and MacBooks: It also collects income from services like the App Store, iCloud, and Apple TV. Revenue from each of these gets its own budget line in Apple’s reports, and sales growth here is strong, hitting an all-time high last quarter.

Services made up $23.8 billion of the total $90.8 billion Apple took in during the second quarter of fiscal 2024 (which ended March 30). That’s a significant portion, so strong growth here is meaningful. Keep an eye out for whether the company can continue to grow this segment.

Should you invest $1,000 in Apple right now?

Before you buy stock in Apple, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Apple wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $830,777!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

American Express is an advertising partner of The Ascent, a Motley Fool company. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Johnny Rice has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Berkshire Hathaway, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

3 Reasons Apple Stock Is a Buy and Hold was originally published by The Motley Fool